GFiber + Astound Broadband The Birth of America’s Third National Broadband Provider

Market Impact Analysis | Competitive Overlap | MSA Battlefield Report

This Changes Everything

The GFiber-Astound merger (backed by Stonepeak) announced on March 11, 2026, resets the US Broadband market.

It also fundamentally restructures Alphabet’s relationship with the “pipes.”

The Deal Structure:

Ownership: Stonepeak takes the majority stake. Alphabet retains a “significant minority” interest. Financial terms undisclosed.

Leadership: The GFiber management team (led by CEO Dinni Jain, former Time Warner Cable / Insight Communications) will run the combined entity.

Footprint: The combination creates a 7.11 million-location national broadband platform across 26 states, combining GFiber’s high-growth metro builds with Astound’s large, established presence in NYC, Chicago, D.C., Houston, and the Pacific Northwest.

Overlap: Minimal - only ~109,000 locations in three Texas counties. The merger is almost entirely additive.

New CEO (Astound): Ettienne Brandt, former EVP Commercial at Frontier Communications, was named Astound CEO on March 17, 2026, to lead integration preparation. The GFiber executive team will lead the combined company post-close.

Expected Close: Q4 2026, subject to regulatory approvals.

What It Proves: The “Waymo-ization” of Google Fiber

Alphabet is no longer willing to carry the capital intensity of a national ISP on its own balance sheet. With projected capex of $185 billion in 2026 aimed at AI data centers and cloud infrastructure, the residential fiber business - capital intensive, slow-return, hyper-local - no longer fits a company whose priorities are planetary-scale AI workloads. By moving to a minority stake, Alphabet gets:

• Off-Balance Sheet Scaling: The significant capex required to fight Comcast and AT&T is now Stonepeak’s capital allocation problem.

• Operational Independence: GFiber can now raise its own debt and equity like a standalone infrastructure company, not a search engine’s side project.

• M&A Velocity: As part of a larger PE-backed entity, the combined company can acquire regional players far faster than Google’s internal processes would ever allow.

This move suggests Alphabet views fiber more as a financial asset and market catalyst than a necessary internal piece of the AI stack. They have decided they don’t need to own the last mile to benefit from it. They would rather own 30% of a national winner than 100% of a regional niche player.

Sources: Stonepeak/GFiber Press Release (Mar 11, 2026); Astound/BusinessWire CEO Announcement (Mar 17, 2026); Light Reading (Mar 12, 2026); CNBC (Mar 11, 2026); Fierce Network (Mar 12, 2026); Alphabet Q4 2025 Earnings Call

The Competitive Overlap: Who Is Most Exposed?

According to New Street Research analysis (March 2026), the competitive overlap for the combined GFiber-Astound entity is highest against AT&T- even more so than Comcast and Charter. Over half of the NewCo footprint will be a direct, house-by-house street fight with AT&T Fiber.

|

Competitor |

Footprint

Overlap |

Homes at Risk |

|

AT&T |

53% |

~3.77 Million |

|

Comcast

(Xfinity) |

46% |

~3.27 Million |

|

Charter

(Spectrum) |

43% |

~3.05 Million |

|

Verizon |

22% |

~1.56 Million |

|

Altice USA

(Optimum) |

~15-20% |

~1.1-1.4

Million |

Table 1. Competitive footprint overlap with GFiber-Astound combined entity (Source: New Street Research, March 2026)

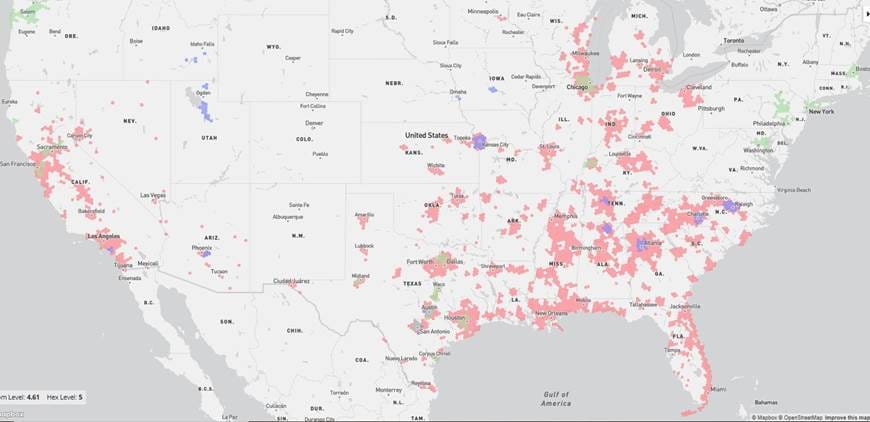

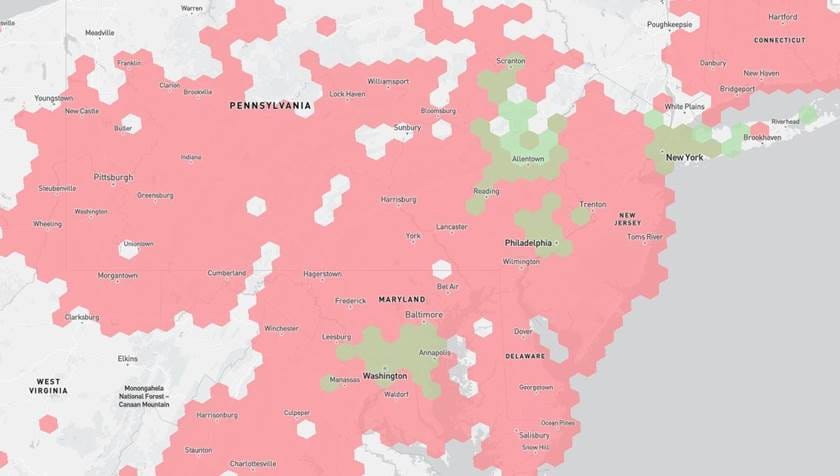

Figure 1. FCC Broadband Map - National view: GFiber (blue/purple) + Astound (green) footprint vs. AT&T Fiber (pink/red). The 53% overlap is concentrated across the Southeast, Texas, and Midwest. Source: FCC Broadband Map, Dec 2024 data.

Comcast: The Urban Target

Comcast is at the greatest numerical risk because Astound’s legacy brands (RCN and Grande) were built specifically to overbuild Comcast in high-density markets. In cities like Chicago, Washington D.C., and Philadelphia, customers who previously viewed Astound as the “budget alternative” will now see a GFiber-managed network offering 3 Gig symmetrical speeds at transparent, no-contract pricing. We estimate Comcast could see a 150-200 basis point increase in churn in metropolitan markets where the GFiber / Astound migration hits first. Over 3.2 million Comcast passings are now in direct competition with a Stonepeak-funded, GFiber-managed competitor.

Charter: The Texas & California Pincer Movement

Charter faces a geographic pincer. GFiber was already attacking Charter in Austin and Mesa; now they have Astound’s assets across Texas and the Pacific Northwest. Charter has been leaning on mobile bundling (Spectrum One) to suppress churn, but GFiber’s “no-contract, no-nonsense” pricing is the direct antithesis of Charter’s complex promotional bundles. Charter is particularly vulnerable in the Texas Triangle (Austin / San Antonio / Houston), where the combined entity will have the most densified fiber footprint in the state outside of AT&T. We expect Charter’s broadband penetration in Austin to drop from an estimated ~45% to sub-35% by 2028.

AT&T: The “Fiber-on-Fiber” War

AT&T has the highest overlap percentage at 53%. More than half of the NewCo footprint will be a direct fiber-on-fiber fight with AT&T - the kind of competition that historically leads to ARPU destruction. The pricing gap is real: GFiber offers 1 Gig at $70 flat versus AT&T at $80 (after discounts); 2 Gig at $100 versus $125; 5 Gig at $125 versus $155. Over a year, an AT&T customer pays a $120-$360 premium for equivalent symmetrical speeds. In an era of persistent inflation and budget-conscious consumers, that is a meaningful churn vector.

AT&T’s primary defense is convergence - the 42% of fiber households who also take AT&T wireless. But the NewCo has a counter: Astound already operates an MVNO through T-Mobile. Under GFiber management with Stonepeak’s balance sheet, a “GFiber Mobile” bundle that undercuts AT&T’s converged pricing becomes a credible threat.

Altice USA: The Casualty

If there is a single casualty of this merger, it is Altice. Already struggling with high leverage and a slow fiber transition, Altice faces the NewCo’s presence in the NYC/New Jersey corridors - Altice’s only remaining cash-cow territory. In areas where GFiber / Astound upgrades to 5 Gig symmetrical, Altice’s legacy HFC network simply cannot compete. We project Altice could lose 3-5% of its broadband base in these overlap zones by 2028.

Sources: New Street Research, Barden & Harlalka (Mar 2026); Light Reading (Mar 12, 2026); Comcast Q4 2025 Earnings; Charter Q4 2025 Earnings

The MSA / DMA Battlefield Report

National numbers are a vanity metric. Market-level density is the only thing that drives churn and ROIC. The NewCo footprint is a surgical strike on the highest-ARPU ZIP codes in America.

|

Market

(MSA/DMA) |

Brand

Presence |

Incumbent at

Risk |

Risk Level |

|

Chicago, IL |

RCN (Astound)

+ GFiber |

Comcast /

AT&T |

CRITICAL |

|

Austin /

San Antonio, TX |

Grande

(Astound) + GFiber |

Charter /

AT&T |

CRITICAL |

|

New York

City / NJ |

RCN (Astound) |

Comcast /

Altice |

HIGH |

|

Washington

D.C. / NoVA |

RCN (Astound) |

Comcast /

Verizon |

HIGH |

|

San

Francisco / Oakland |

Wave (Astound)

+ GFiber |

Comcast /

AT&T |

HIGH |

|

Houston /

Dallas, TX |

Grande

(Astound) |

Charter /

AT&T |

HIGH |

|

Seattle /

Portland |

Wave (Astound)

+ GFiber |

Comcast /

Ziply |

MODERATE |

|

Charlotte /

Raleigh, NC |

GFiber |

Charter /

AT&T |

HIGH |

|

Phoenix /

Mesa, AZ |

GFiber |

Cox / AT&T

(Lumen) |

HIGH |

|

Atlanta, GA |

GFiber |

Comcast /

AT&T |

MODERATE |

|

Denver, CO |

GFiber

expansion |

Comcast /

AT&T (Lumen) |

HIGH |

Table 2. MSA / DMA Battlefield Report - Primary market overlap and incumbent risk assessment (March 2026)

Deep Dive: The Texas Triangle - The Charter Pincer

Texas is the epicenter of this conflict. The GFiber-Astound combination has its highest concentration in Texas and Illinois. The following FCC broadband map views illustrate the pincer in real time.

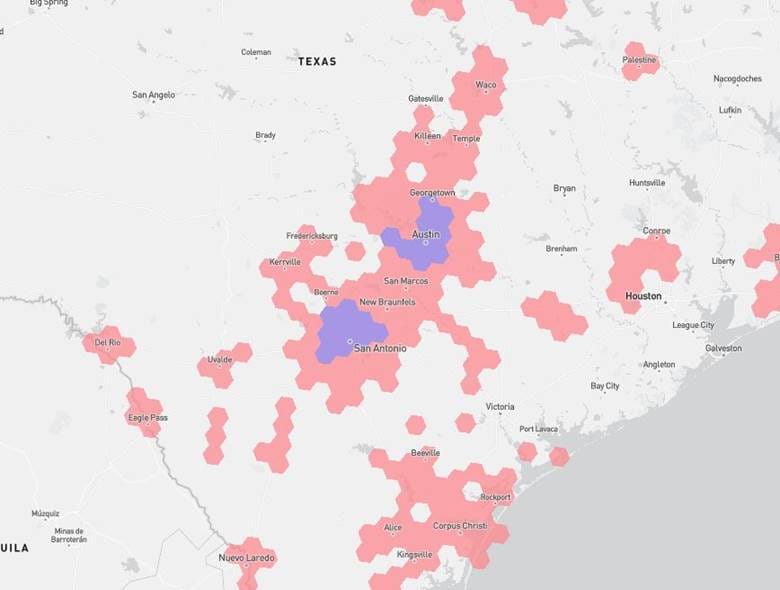

First, Charter’s (Spectrum) Texas footprint with only GFiber overlap. GFiber’s presence (purple) is concentrated in Austin and San Antonio, sitting directly inside Charter’s sprawling coverage (pink):

Figure 2. FCC Broadband Map - Texas: Charter/Spectrum (pink) vs. GFiber only (purple). GFiber's footprint is concentrated in Austin and San Antonio, creating direct overlap in Charter's most profitable growth corridors. Source: FCC Broadband Map, Dec 2024 data.

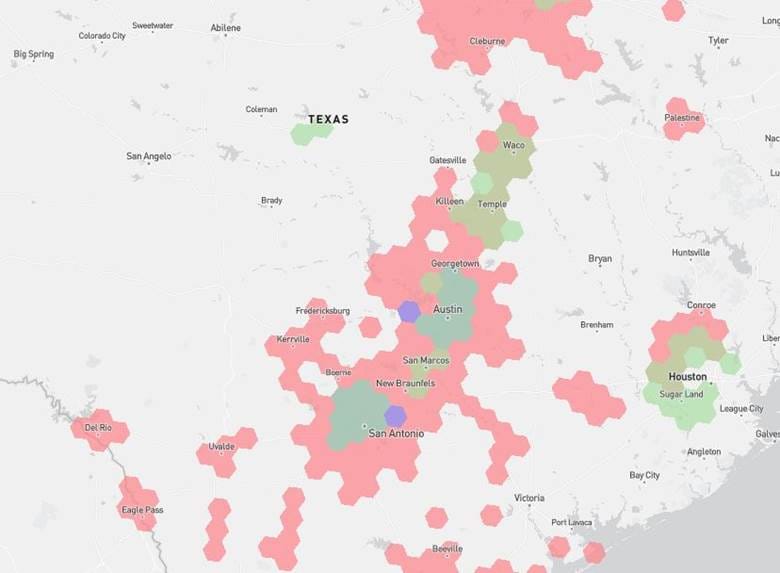

Now add Astound (Grande) to the picture. The green hexagons fill in the corridors between Austin, San Antonio, Houston, and the I-35 corridor - completing the pincer movement:

Figure 3. FCC Broadband Map - Texas: Charter/Spectrum (pink) vs. GFiber (purple) + Astound/Grande (green). The addition of Astound fills the Houston, Waco/Temple/Killeen, and San Marcos corridors, creating a continuous competitive footprint across the entire Texas Triangle. Source: FCC Broadband Map, Dec 2024 data.

In Austin and San Antonio, the combined entity now passes roughly 85% of the same homes that AT&T is targeting for fiber upgrades. This transforms a “monopoly fiber” market into a “duopoly fiber” market - which typically halves the expected ROIC. Charter is simultaneously fighting two fiber giants (AT&T and NewCo) in its most profitable growth markets.

Deep Dive: Chicago - The Comcast Squeeze

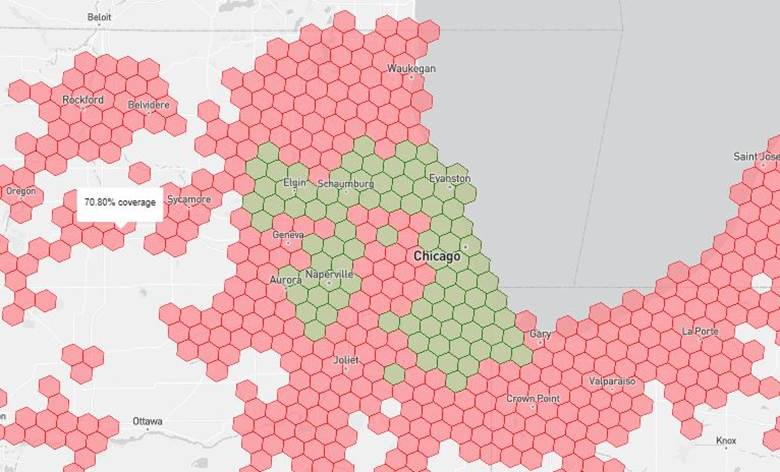

In the Midwest, Astound (via RCN) already has deep fiber / coax assets in high-density MDUs (Multi-Dwelling Units). The FCC map shows the overlap clearly - Astound’s coverage (green) sits directly inside Comcast’s Chicago footprint (pink / red):

Figure 4. FCC Broadband Map - Chicago MSA: Comcast (pink/red) vs. GFiber + Astound/RCN (green). Astound's RCN footprint blankets Chicago's urban core and northern suburbs, creating 70%+ coverage overlap in Comcast's highest-margin MDU territory. Source: FCC Broadband Map, Dec 2024 data.

GFiber management is reportedly planning to “overbuild their own overbuild,” replacing Astound’s older coax with 10-Gig capable fiber. In a Chicago high-rise, a $70/month 3-Gig symmetrical GFiber plan (no contract) makes Comcast’s Triple Play bundle an anchor, not a value proposition. Comcast generates its highest margins in these dense urban centers.

Deep Dive: NYC, Philadelphia & Washington D.C. - The Northeast Corridor

Astound’s RCN brand stretches across the entire Northeast power corridor - from New York City through Philadelphia and into the D.C. metro area. This is Comcast’s home turf:

Figure 5. FCC Broadband Map - Northeast Corridor: Comcast (pink) vs. Astound/RCN (green) from New York through Philadelphia to Washington D.C. The overlap in Lehigh Valley (PA), Northern NJ, and the D.C./Baltimore metro is extensive, hitting Comcast and Altice in their most concentrated subscriber bases. Source: FCC Broadband Map, Dec 2024 data.

For Altice (Optimum), this is particularly dangerous. Altice’s only remaining cash-cow territory is the NYC / Long Island/NJ corridor, and the NewCo now has a direct presence there. Combined with GFiber’s brand upgrade and Stonepeak’s capital, we project a 4% total subscriber loss for Altice in these overlap areas within 24 months.

Sources: FCC Broadband Map (broadbandmap.fcc.gov), Dec 2024 data vintage; New Street Research Broadband Insights (Mar 2026); Light Reading market analysis (Mar 12, 2026)

The AT&T-Lumen Dimension: A Land Grab Meets a Street Fight

AT&T’s $5.75 billion acquisition of Lumen’s Mass Markets fiber business (closed February 2, 2026) was a textbook land grab- and the overlap with AT&T’s legacy wireline footprint was effectively 0%.

What AT&T Acquired

• Homes Passed: 4 million fiber locations

• Active Subscribers: 1.1 million

• Implied Penetration: ~27% (significant runway versus AT&T’s 40%+ in legacy markets)

• Geographic Reach: 11 states, primarily Pacific Northwest, Mountain West, and Midwest

• Key Metros: Denver, Seattle, Phoenix, Salt Lake City, Portland, Minneapolis, Las Vegas

• Footprint Expansion: AT&T goes from 21-state legacy wireline to 32 states

The Convergence Multiplier

The real math is not the $70/month fiber bill - it is the wireless attach rate. In AT&T’s legacy fiber footprint, 42% of fiber households also take AT&T wireless. In the acquired Lumen territories, wireless attach is under 20%. That gap, from sub-20% to a target of 42%+ - represents millions of potential wireless cross-sells. AT&T can now walk into a Lumen fiber home and offer a converged bundle that directly attacks T-Mobile and Verizon’s wireless stronghold in the West.

The Collision Course

Here is the strategic irony: by expanding into Lumen’s territories (Denver, Phoenix, Seattle), AT&T has walked directly into the crosshairs of the GFiber-Astound NewCo. In Denver, Comcast is now fighting AT&T Fiber and GFiber/Astound simultaneously- a three-way war that typically ends in a price race to the bottom. For AT&T, the “bull case” was that they would eventually own a fiber monopoly in their footprint as cable became obsolete. The GFiber-Astound merger kills the monopoly thesis. AT&T now has to fight a well-capitalized, technically competitive fiber rival for every high-value customer in Texas and Chicago.

Sources: AT&T Q4 2025 Earnings Release (Jan 28, 2026); AT&T/Lumen Close Announcement (Feb 2, 2026); Light Reading (Jan 28, 2026)

Scale Check: Homes Passed Comparison

In the cable and telecom world, passings (total homes where service is available) are the Total Addressable Market. Here is how the NewCo stacks up against the incumbents:

Table 3. U.S. broadband providers - Homes passed comparison and risk assessment (March 2026)

While 7.1 million passings is only ~12% of Comcast’s total size, you cannot evaluate this on a national basis. You must look at it market by market. In the 26 states where the NewCo operates, it is not a niche player - it is a Primary Competitor. This merger effectively “professionalizes” the cable industry’s most aggressive regional overbuilder (Astound) by giving them the best management team in residential broadband (GFiber) and a patient infrastructure capital partner (Stonepeak).

The Pricing War: Death of the Promo

Watch for the “GFiber way” to infect every Astound market. Astound historically operated like a traditional cable company: low introductory prices, steep increases, hidden fees. GFiber operates on flat, transparent pricing with no contracts. If they successfully migrate Astound’s 1M+ subscribers to the GFiber pricing model, they will cause what we call a “churn-pocalypse” for Comcast in Tier-1 cities.

2026 Pricing Comparison: GFiber vs. AT&T Fiber

• 1 Gig: GFiber $70 (flat) vs. AT&T $80 (after autopay/paperless discounts) - $120/year premium

• 2 Gig: GFiber $100 vs. AT&T $125 - $300/year premium

• 5 Gig: GFiber $125 vs. AT&T $155 - $360/year premium

The biggest risk to the incumbents is not just lost subscribers - it is ARPU compression. To keep customers from jumping to a $70/month 1-Gig symmetrical GFiber plan, Comcast, Charter, and AT&T will have to lower prices or increase speeds at no additional cost. That is a margin killer.

The Hardware Roadmap

GFiber’s 20 Gig trials and Wi-Fi 7 rollouts will now be exported to Astound’s millions of existing customers. Expect a large-scale “refresh” campaign where Astound customers are migrated to “GFiber Powered” plans - a brand upgrade that simultaneously upgrades the network and resets the competitive narrative in every market.

The Net Gain Verdict

The GFiber-Astound merger creates a Triple Threat that has not existed in American broadband before:

• The Brand: Google’s “cool factor,” simplicity, and industry-leading NPS scores.

• The Pipe: Astound’s large, established urban footprint- 4.5 million locations in the highest-ARPU ZIP codes in America.

• The Bank: Stonepeak’s long-term infrastructure capital. Private equity does not care about quarterly earnings calls the way Comcast and Charter do. Stonepeak cares about long-term IRR. They will spend $2,000 per home passed to take a customer from Xfinity if it builds long-term asset value.

For the incumbents, the era of gentlemanly competition is over.

This is a land war for the last mile.

Vulnerability Rankings

• #1 Altice USA: Weakest balance sheet, most distracted by restructuring. NewCo presence in NYC/NJ corridors hits Altice’s only remaining cash-cow territory. Projected 4% total sub loss in overlap areas within 18 months.

• #2 Comcast: Greatest absolute exposure. Over 3.2 million passings now face a Stonepeak-funded, GFiber-managed competitor. Projected exposure of 150-200 bps churn increase in affected metros.

• #3 AT&T: Fighting a “peer.” The 53% footprint overlap and $120-$360/year pricing gap threaten ARPU growth in the Texas Triangle and Chicago. The fiber monopoly thesis runs into a wall.

• #4 Charter: The Texas pincer movement and mobile bundle vulnerability. Broadband penetration in Austin projected to potentially drop from ~45% to sub-35% by 2028.

The Astound deal highlights that scale truly matters in the broadband business.

By mergingwith Astound, GFiber skips 10 years of trenching and buys its way into the biggest markets in America.

For Alphabet, this is a masterclass in risk mitigation; they keep the brand glory and the AI-enablement upside, but hand the dirt and shovel work to Stonepeak.

Meanwhile, Stonepeak essentially “buys” a premium best-in-class technology brand asset, positioning itself at / near the top, of the highly competitive broadband market. The implications for the entire broadband industry are meaningful and could prove to be quite profound.

• • •

Analysis prepared March 2026. All data sourced from public earnings releases, SEC filings, press releases, New Street Research, FCC Broadband Map, and industry analyst reports.